Post-War Relief Rally Begins but Experts Warn “The Economic Damage Isn’t Going Away Anytime Soon”

A post-war relief rally is beginning to take shape across global markets, with investors reacting positively to reduced uncertainty. However, many experts caution that while markets may bounce back quickly, the deeper economic effects of the conflict are likely to linger.

Markets Are Reacting to Immediate Relief

As tensions ease, investors begin moving back into stocks and other risk assets. This creates a surge in buying activity driven by improved sentiment. The rally often reflects relief rather than strong economic fundamentals. Prices can rise quickly as fear fades. However, this optimism is still cautious beneath the surface. Markets are responding to the pause, not a full recovery.

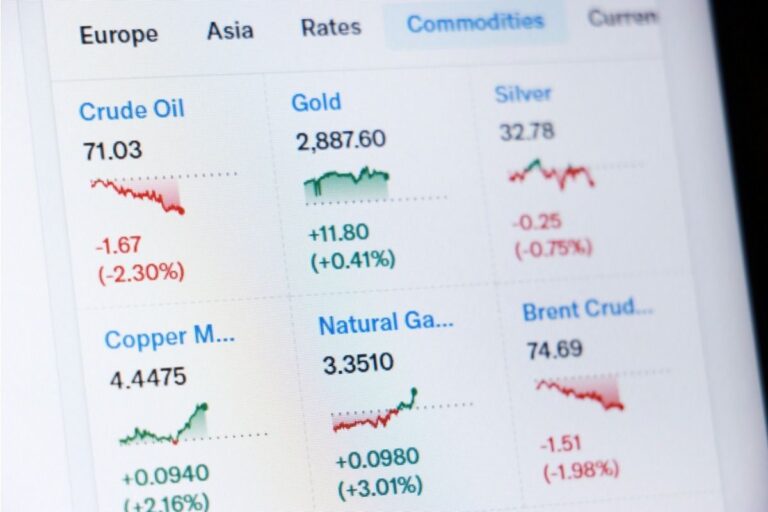

Oil Prices May Cool but Effects Remain

Energy markets tend to stabilize once supply risks decline. Lower oil prices can ease pressure on fuel and transportation costs. However, earlier price spikes may have already affected businesses and consumers. These effects don’t disappear instantly. Costs that increased during the conflict may remain elevated. The cooling of oil helps, but it doesn’t erase past impact.

Inflation Damage Takes Time to Reverse

When prices rise across multiple sectors, they rarely drop back quickly. Businesses often keep prices higher to protect margins. Consumers may see slower increases, but not necessarily lower prices. This makes the impact of inflation long-lasting. Even after conditions improve, the cost of living can remain high. Recovery in pricing tends to be gradual.

Supply Chains Need Time to Recover

During the conflict, supply chains may have adjusted to disruptions and higher costs. These systems don’t return to normal immediately. Shipping routes, contracts, and inventory strategies take time to stabilize. Delays and inefficiencies can persist for a while. This keeps pressure on pricing and availability. Recovery is a process, not an instant reset.

Businesses Remain Cautious

Even with improving conditions, many companies avoid making quick changes. They may hold back on hiring, expansion, or investment. This caution slows down overall economic recovery. Businesses need consistent stability before increasing activity. Short-term relief does not guarantee long-term confidence. Decisions remain careful and measured.

Consumers Continue to Feel the Pressure

Households may still deal with higher costs even after markets recover. Wages and spending patterns take time to adjust. This creates a gap between market optimism and everyday reality. Financial pressure does not disappear with a rally. The effects of earlier increases remain noticeable. Consumer confidence improves slowly.

Central Banks May Stay Conservative

Policymakers often wait for clear signs of stable inflation before adjusting policies. Interest rates may remain higher for longer. This affects borrowing, investment, and spending. Even with better market conditions, policy changes can lag behind. Stability is prioritized over speed. Economic support is adjusted carefully.

The Recovery Will Be Uneven

Different sectors recover at different speeds. Financial markets may improve quickly, while real economic conditions take longer. Some industries benefit immediately, while others continue to struggle. This creates a mixed recovery pattern. Not all improvements are felt at the same time. The overall picture remains complex.

Relief Is Real, but So Is the Impact

The rally shows that confidence is returning, but it does not mean the damage is gone. Economic effects from the conflict will continue to play out over time. Recovery will depend on stability, policy, and global conditions. The current optimism reflects hope, not full resolution.